Skip to content

Courses

Blog Posts

Tag:

#equityvaluation

Concept of Operating (De) Leverage explained through movies!

Sep 10, 2025

How to estimate market size–top-down and bottom-up?

Sep 9, 2025

Resources for Investors, Equity Analysts, and Strategy Consultants

Sep 9, 2025

How to do Fundamental Analysis of General/Health/Property & Casualty Insurers?

Sep 9, 2025

Resources to help investors, aspiring equity research analysts and finance focused strategy consultants

Sep 9, 2025

Allison Transmission: Equity Research and Valuation

Sep 8, 2025

Reverse DCF is a quick and dirty way to assess if a company is over or undervalued

May 27, 2025

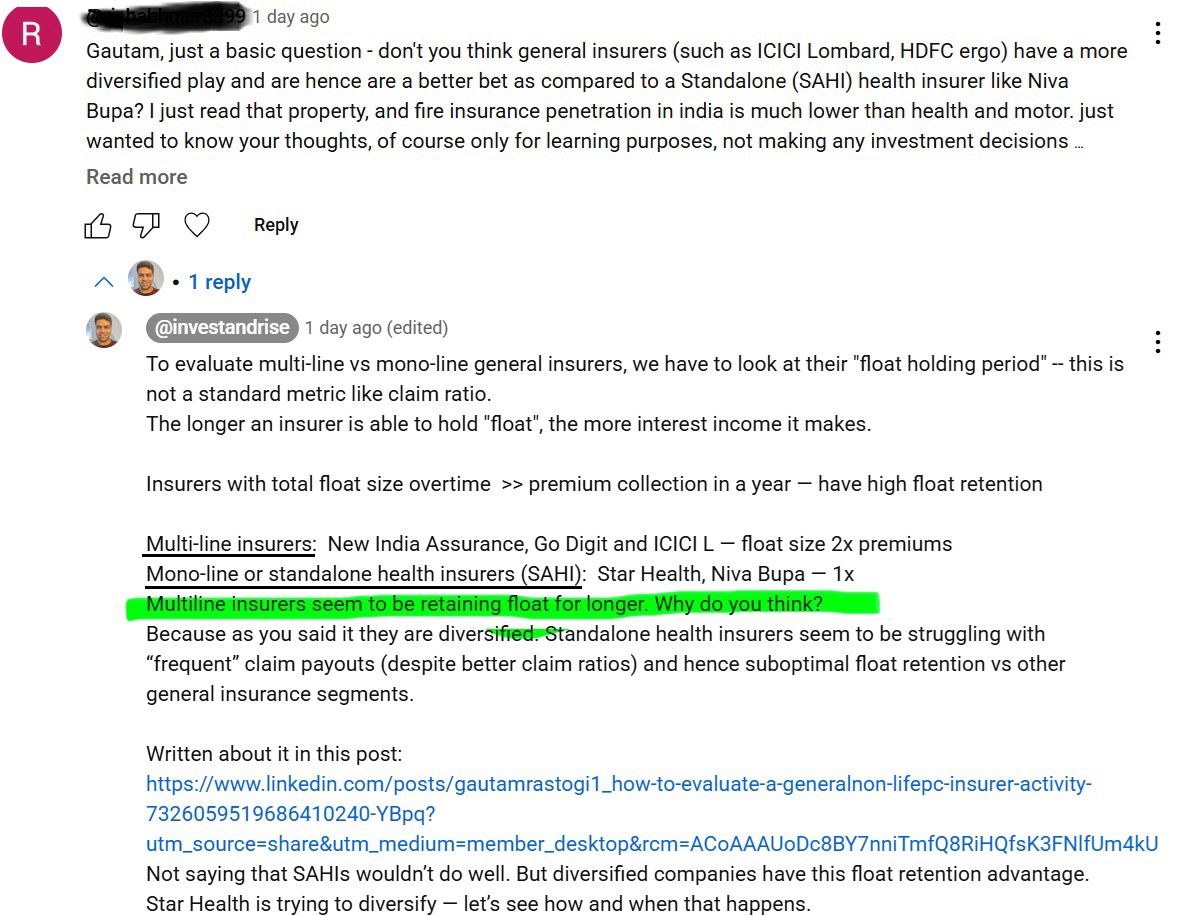

ICICI Lombard, HDFC Ergo Vs Star Health, Niva Bupa

May 27, 2025

How to analyze company earnings con call?

May 27, 2025

How to analyze a general insurance business using Warren Buffett’s method?Learn to spot 🍋

May 27, 2025

1

2

3

…

5

Next Page

Connect with us

Please enable JavaScript in your browser to complete this form.

Please enable JavaScript in your browser to complete this form.

Name

*

First

Last

or Email Comment

Email

*

Comment or Message

Submit

CLOSE