Skip to content

Courses

Blog Posts

Tag:

#equity

Resources for Investors, Equity Analysts, and Strategy Consultants

Sep 9, 2025

Resources to help investors, aspiring equity research analysts and finance focused strategy consultants

Sep 9, 2025

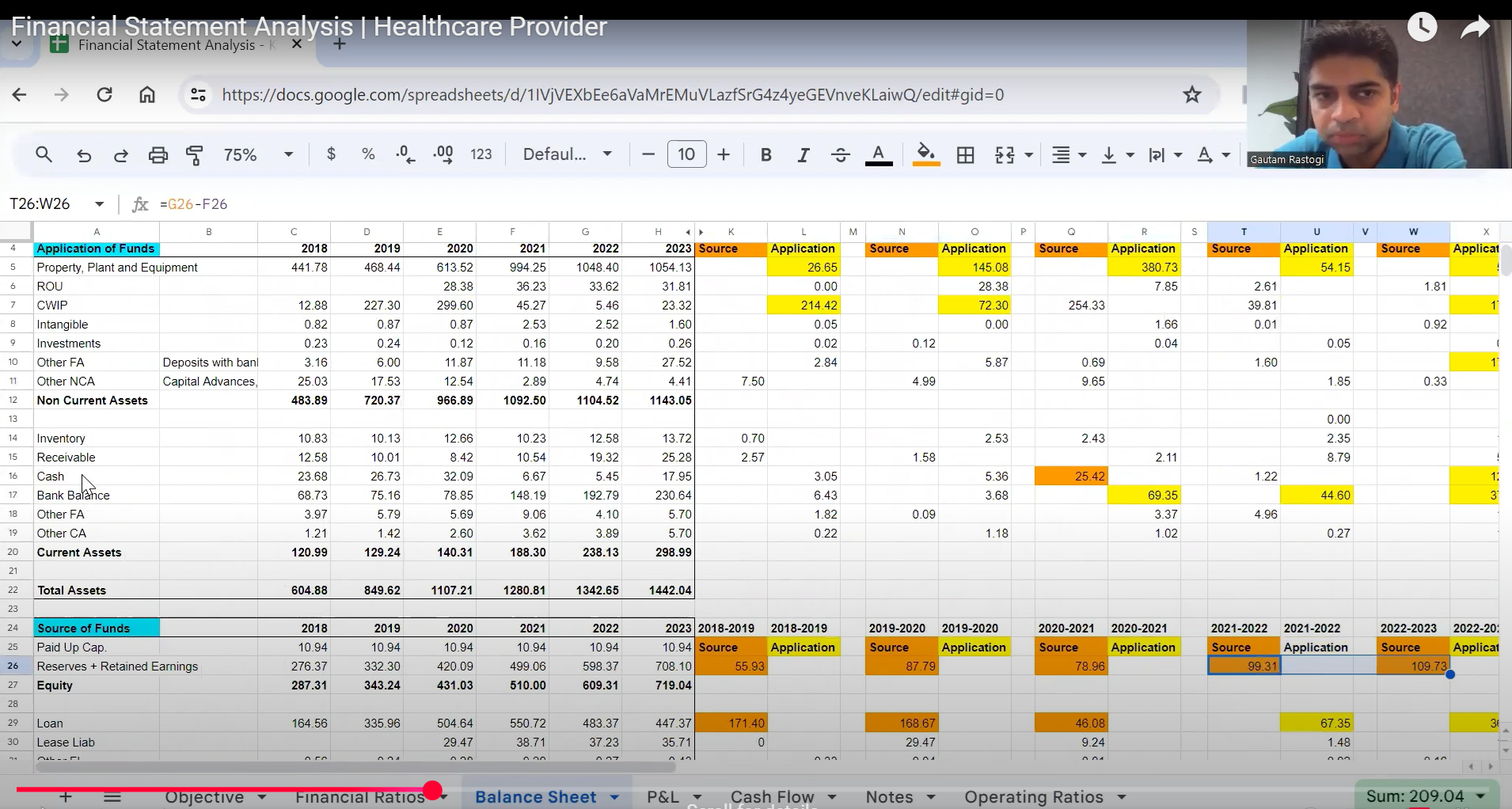

Financial Statement Analysis

Jun 20, 2024

Equity Research | Agarwal Industrial Corp Ltd

Jun 20, 2024

My notes on Rajshree Polypack, a company that makes packaging for F&B industry

Dec 21, 2023

Oriental Carbon and Chemicals – Indian company operating in an Oligopoly

Jun 30, 2023

Costco Equity Valuation

Jun 13, 2020

Value in Facebook

Jan 2, 2020

Bandhan and Gruh Merger Valuation

Dec 15, 2019

Bandhan Bank Valuation (just prior to merger with Gruh)

Dec 4, 2019

1

2

Next Page

Connect with us

Please enable JavaScript in your browser to complete this form.

Please enable JavaScript in your browser to complete this form.

Name

*

First

Last

Email

*

Message Name or

Comment or Message

Submit

CLOSE