Skip to content

Courses

Blog Posts

Tag:

#DCF

Concept of Operating (De) Leverage explained through movies!

Sep 10, 2025

How to estimate market size–top-down and bottom-up?

Sep 9, 2025

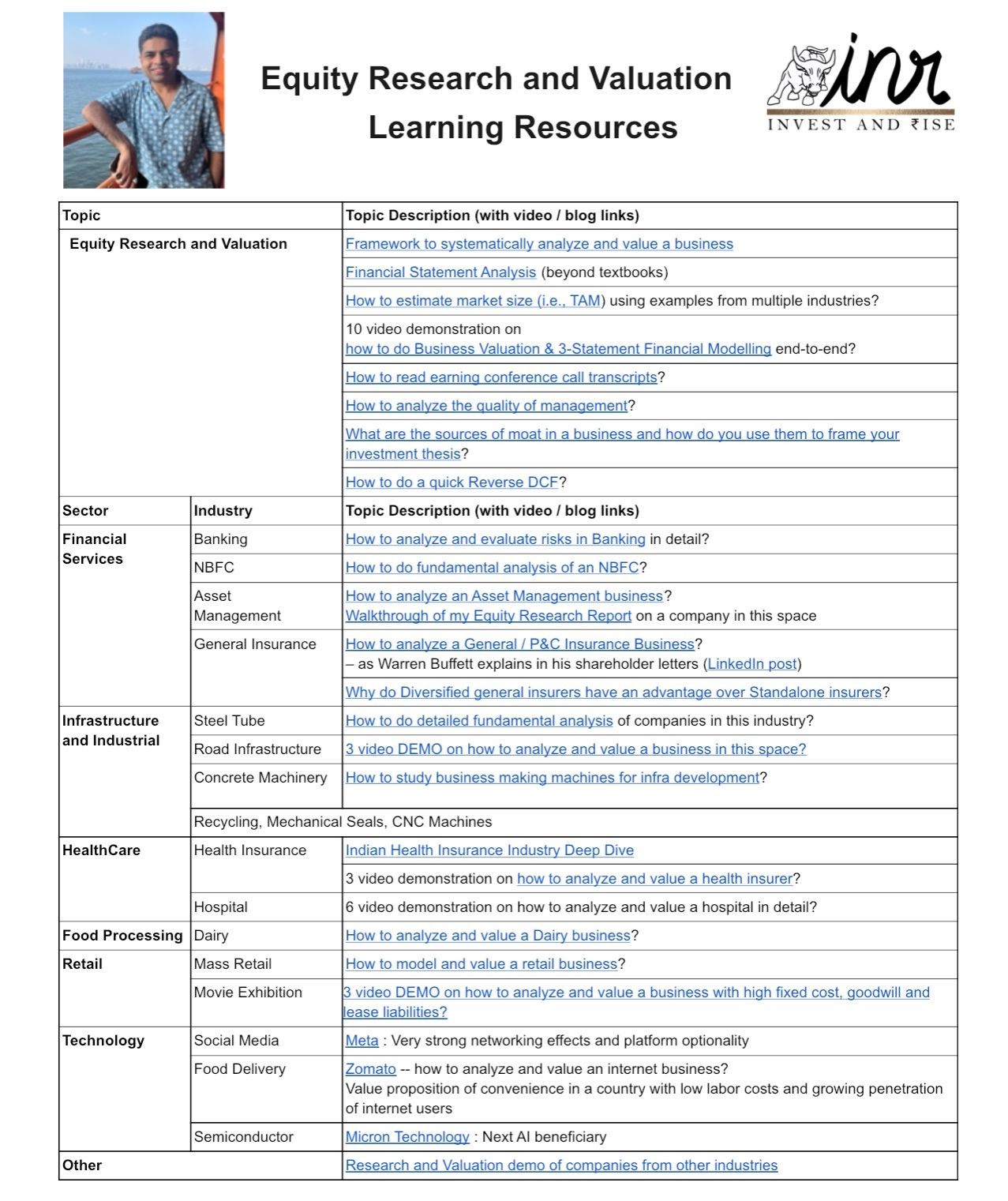

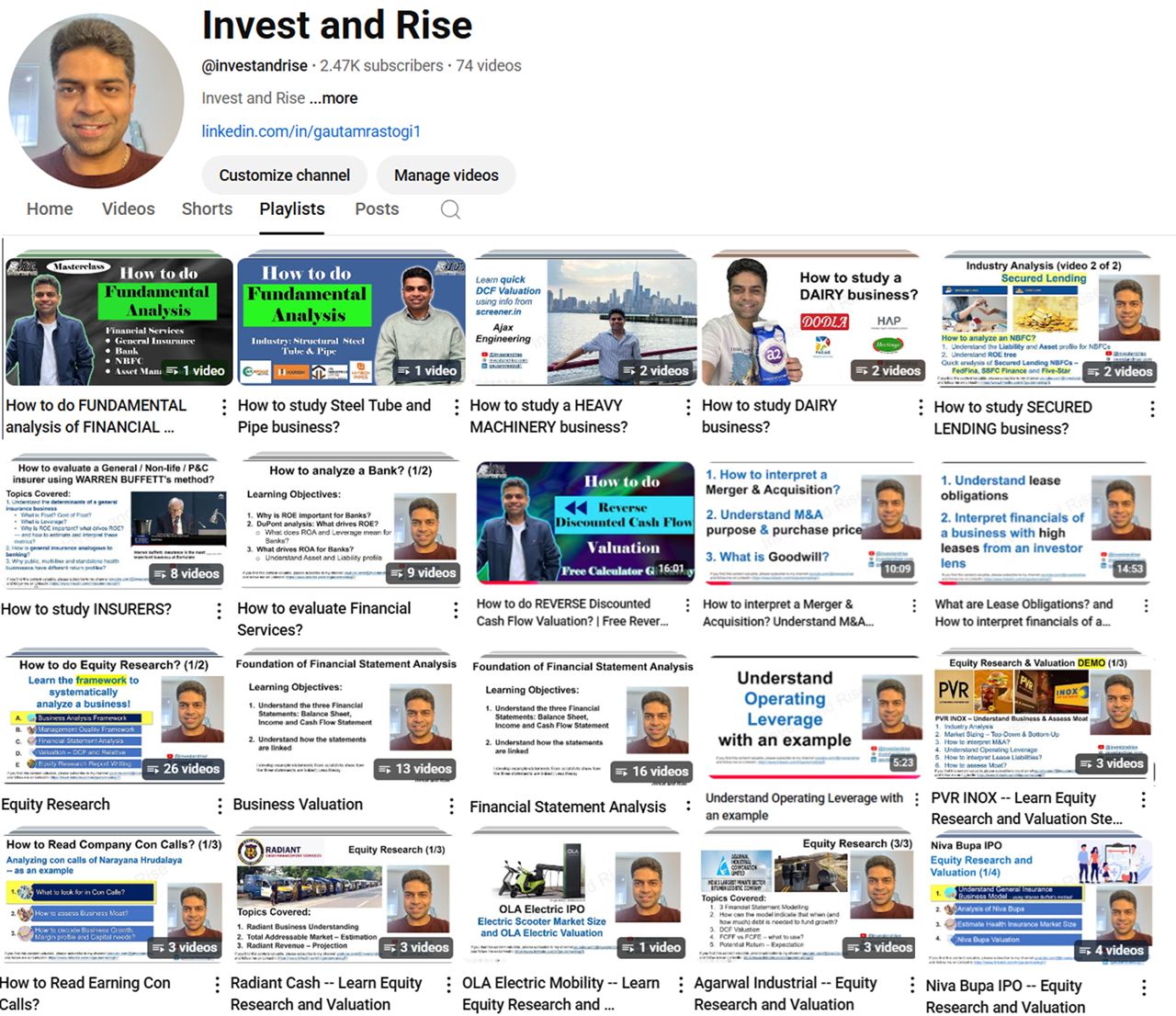

Resources for Investors, Equity Analysts, and Strategy Consultants

Sep 9, 2025

Resources to help investors, aspiring equity research analysts and finance focused strategy consultants

Sep 9, 2025

Reverse DCF is a quick and dirty way to assess if a company is over or undervalued

May 27, 2025

𝗟𝗲𝗮𝗿𝗻 𝗾𝘂𝗶𝗰𝗸 𝗗𝗖𝗙 𝗩𝗮𝗹𝘂𝗮𝘁𝗶𝗼𝗻 𝘂𝘀𝗶𝗻𝗴 𝗶𝗻𝗳𝗼 𝗳𝗿𝗼𝗺 𝘀𝗰𝗿𝗲𝗲𝗻𝗲𝗿.𝗶𝗻

May 27, 2025

PVR INOX Equity Research and Valuation DEMO

Mar 20, 2025

Interested in learning equity research and valuation step by step – through practical examples?

Mar 20, 2025

Balance sheets are forgotten during Bull markets!

Mar 19, 2025

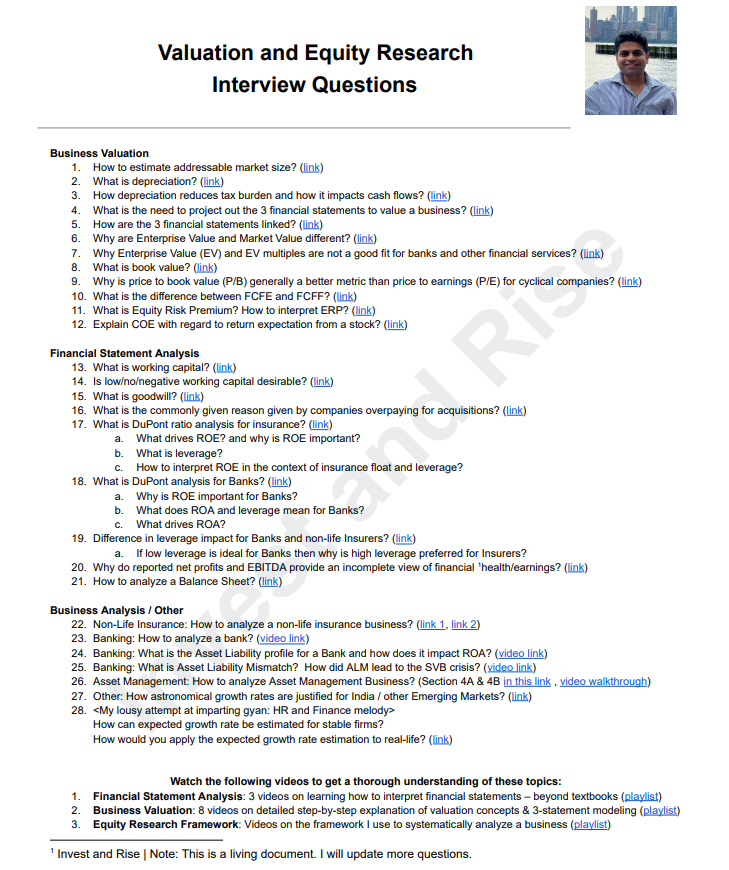

Valuation and Equity Research – Interview Questions

Jul 2, 2024

1

2

Next Page

Connect with us

Please enable JavaScript in your browser to complete this form.

Please enable JavaScript in your browser to complete this form.

Name

*

First

Last

Message Comment or

Email

*

Comment or Message

Submit

CLOSE