Skip to content

Courses

Blog Posts

Tag:

#valuation

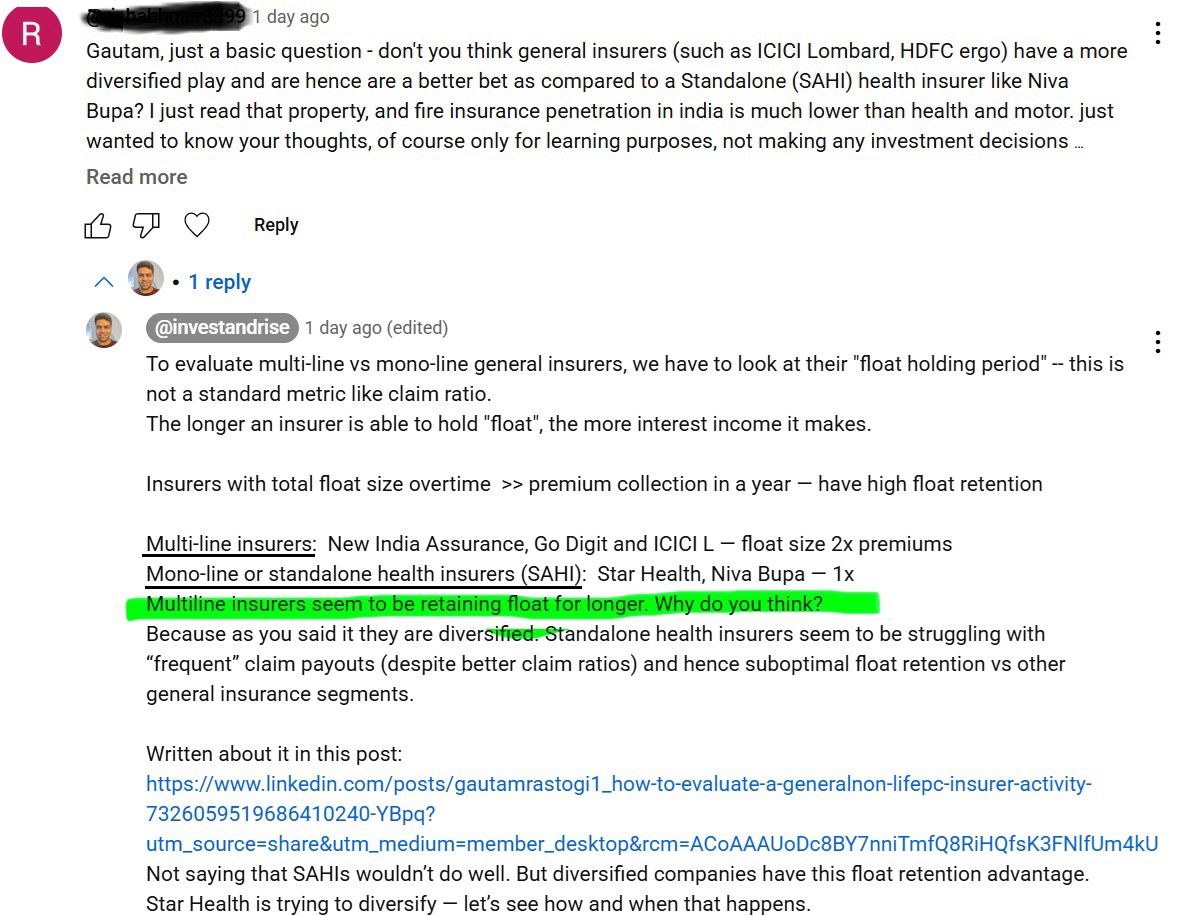

ICICI Lombard, HDFC Ergo Vs Star Health, Niva Bupa

May 27, 2025

How to analyze company earnings con call?

May 27, 2025

How to analyze a general insurance business using Warren Buffett’s method?Learn to spot 🍋

May 27, 2025

“𝙄 𝙨𝙥𝙚𝙣𝙙 𝙢𝙤𝙧𝙚 𝙩𝙞𝙢𝙚 𝙡𝙤𝙤𝙠𝙞𝙣𝙜 𝙖𝙩 𝙗𝙖𝙡𝙖𝙣𝙘𝙚 𝙨𝙝𝙚𝙚𝙩𝙨 𝙩𝙝𝙖𝙣 𝙄 𝙙𝙤 𝙞𝙣𝙘𝙤𝙢𝙚 𝙨𝙩𝙖𝙩𝙚𝙢𝙚𝙣𝙩𝙨. 𝘼𝙣𝙙 𝙒𝙖𝙡𝙡𝙨𝙩𝙧𝙚𝙚𝙩 𝙙𝙤𝙚𝙨 𝙣𝙤𝙩 𝙧𝙚𝙖𝙡𝙡𝙮 𝙥𝙖𝙮 𝙖𝙩𝙩𝙚𝙣𝙩𝙞𝙤𝙣 𝙩𝙤 𝙗𝙖𝙡𝙖𝙣𝙘𝙚 𝙨𝙝𝙚𝙚𝙩𝙨,

May 27, 2025

𝗘𝗻𝗱 𝗼𝗳 𝗮𝗻 𝗲𝗿𝗮!

May 27, 2025

𝗪𝗵𝘆 𝗶𝘀 𝗣/𝗕 𝗮 𝗯𝗲𝘁𝘁𝗲𝗿 𝘃𝗮𝗹𝘂𝗮𝘁𝗶𝗼𝗻 𝗺𝗲𝘁𝗿𝗶𝗰 𝘁𝗵𝗮𝗻 𝗣/𝗘 𝗳𝗼𝗿 𝗕𝗮𝗻𝗸𝘀?

May 27, 2025

Why EV and EV multiples are not a good fit for banks

May 27, 2025

𝗟𝗲𝗮𝗿𝗻 𝗾𝘂𝗶𝗰𝗸 𝗗𝗖𝗙 𝗩𝗮𝗹𝘂𝗮𝘁𝗶𝗼𝗻 𝘂𝘀𝗶𝗻𝗴 𝗶𝗻𝗳𝗼 𝗳𝗿𝗼𝗺 𝘀𝗰𝗿𝗲𝗲𝗻𝗲𝗿.𝗶𝗻

May 27, 2025

𝗡𝗲𝘄 𝗬𝗼𝗿𝗸 🌆 𝗶𝘀 𝗼𝗳𝘁𝗲𝗻 𝗿𝗲𝗳𝗲𝗿𝗿𝗲𝗱 𝘁𝗼 𝗮𝘀 𝘁𝗵𝗲 𝗖𝗼𝗻𝗰𝗿𝗲𝘁𝗲 𝗝𝘂𝗻𝗴𝗹𝗲!

May 27, 2025

𝗛𝗼𝘄 𝘁𝗼 𝗮𝗻𝗮𝗹𝘆𝘇𝗲 𝗮 𝗗𝗔𝗜𝗥𝗬 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀?

May 27, 2025

Previous Page

1

2

3

4

…

6

Next Page

Connect with us

Please enable JavaScript in your browser to complete this form.

Please enable JavaScript in your browser to complete this form.

Name

*

First

Last

Email

*

Comment Message Email

Comment or Message

Submit

CLOSE